What’s the best way to pay off debt?

Debt can help us accomplish goals, like getting a loan for a car or making some upgrades at home, but it’s easy to fall behind if you take on more debt than you can afford to pay back. Experian's 2025 Consumer Credit Review reports the average non-mortgage debt balance is more than $21,000. With credit card interest rates averaging 21% according to the Federal Reserve, it’s important to keep an eye on your balance and make monthly payments before there’s a mountain of unpaid interest in front of you. The good news is that you can regain control and pay down your debts by following one of these three payoff strategies.

GROW your money with a high-yield savings account

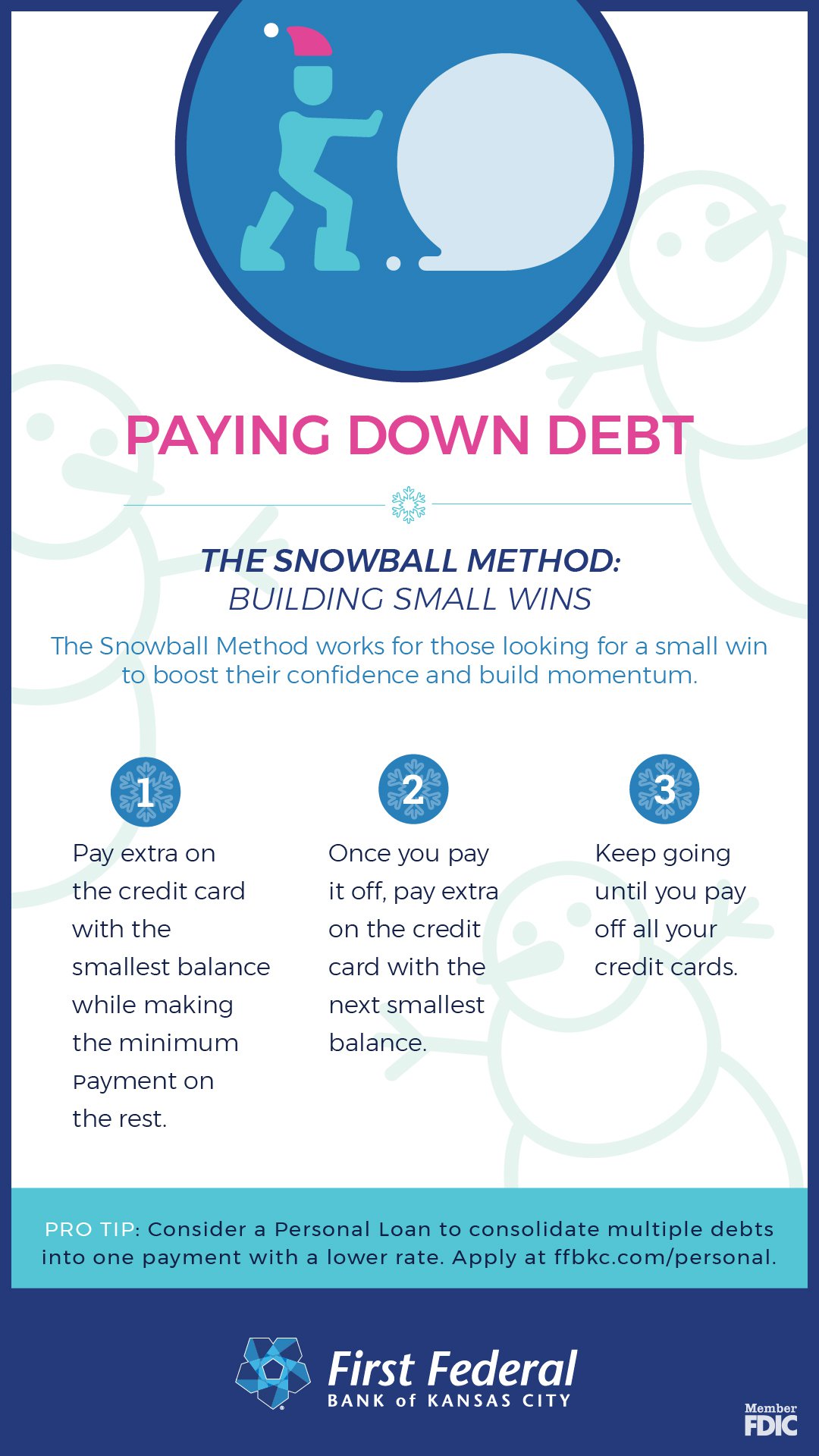

Snowball Method

The gist

With the snowball method, we line up our debts – from smallest to largest - and start knocking them out one by one.

How it works

Say you’re making minimum payments on some of your debts. Put extra effort into paying off the smallest debt first. Then, when that’s paid off, we take the money we were paying towards it and add it toward the payment for the next one. Keep doing the same thing right down the line, snowballing the amount we can pay as we eliminate each debt one by one.

The snowball debt elimination method is empowering. Each debt we successfully knock out gives us more momentum for eliminating the next one and has us feeling the awesome power of our debt-crushing snowball.

Who it’s for

The snowball method is for those of us who know that quick wins will keep us motivated to keep knocking out that debt.

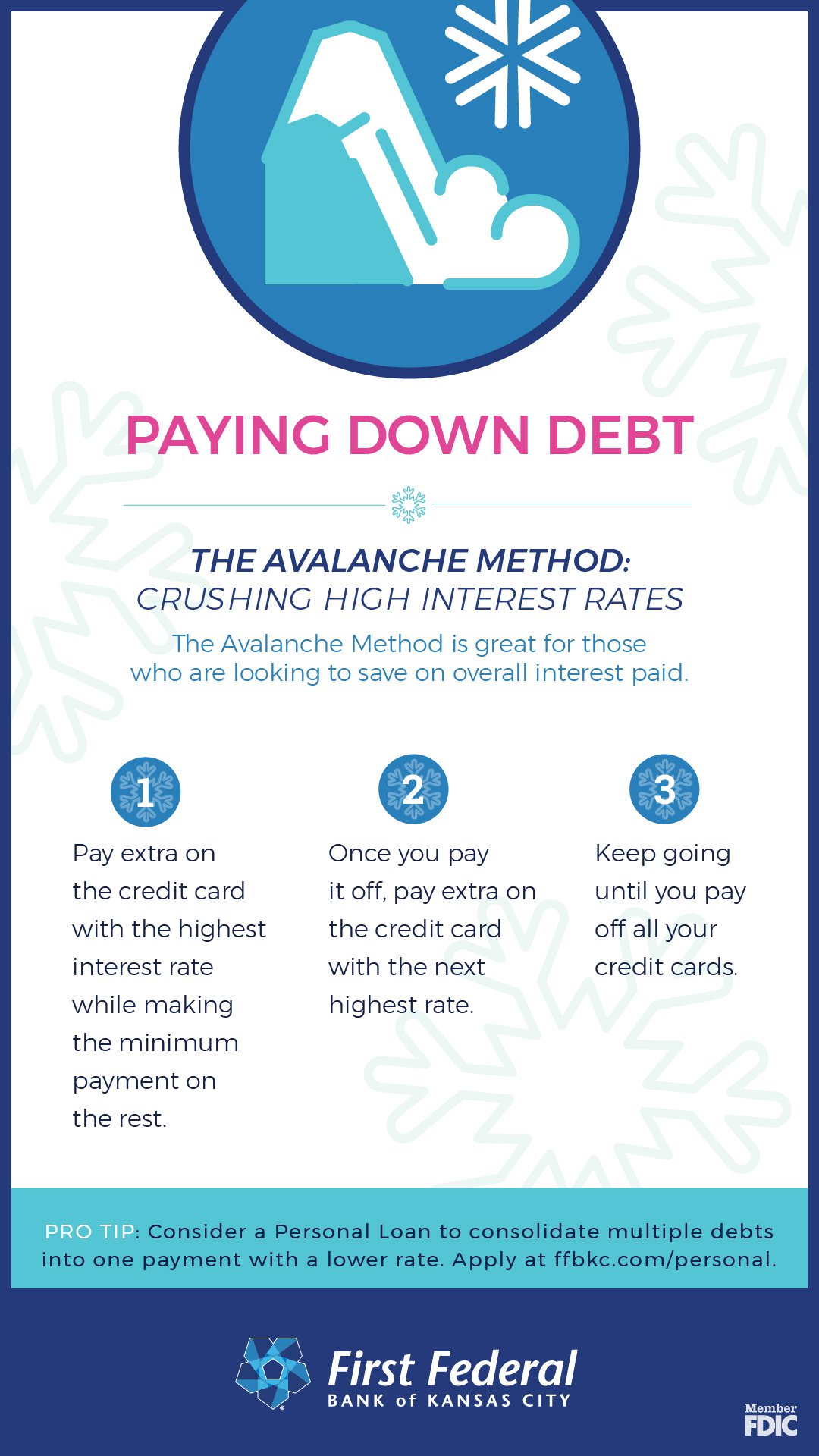

Avalanche Method

The avalanche method is for those of us looking for the most efficient way to eliminate our debt.

The gist

The avalanche method helps eliminate debt by organizing our payments based on interest rates. Just like an avalanche, this method will help sweep away our debt from top to bottom. Plus, it’s going to help us by starting with the debt that will cost us the most, saving us money in the long run.

How it works

Take a look at the terms of all of those loans you’re paying off. List each of them starting with the highest interest rate to the debt with the lowest. We’ll start by focusing first on paying off the highest interest rate. Once we’ve done that, the money we were paying towards it will go to the next highest one, and so on and so forth.

Who it’s for

This is the strategy for those of us who are more analytical and want the most cost-efficient way to eliminate our debt.

Debt Consolidation

Another option is to consolidate your debt into one loan and ideally, secure more favorable terms than the credit card companies could offer. This method works well to reset your focus on just one loan if paying on multiple accounts feels stressful. Plus, if you’re saving on interest payments, you can use the extra funds to pay more than the minimum to pay off the loan faster.

Consolidate debt with your home's equity

Taking out loans or paying on credit cards can be helpful for larger purchases, but multiple accounts and high interest rates may make it difficult to keep up with payments. Take time to develop a debt payoff strategy from the very beginning that works for your budget and goals. Remember, it’s your financial future to control!